Meaning and Fundamentals of Double Entry Book-Keeping 11th BK Commerce Chapter 2 Solutions Maharashtra Board

Balbharti Maharashtra State Board Bookkeeping and Accountancy 11th Solutions Chapter 2 Meaning and Fundamentals of Double Entry Book-Keeping Textbook Exercise Questions and Answers.

Class 11 Commerce BK Chapter 2 Exercise Solutions

1. Answer in one sentence only.

Question 1.

What is a Double Entry System?

Answer:

A system of accounting is which double or two-fold effects of every business transaction are recorded systematically in the books of accounts is called a double-entry book-keeping system.

Question 2.

What is an Account?

Answer:

The summarised record of all transactions related to a person, an institution, an income, and expenditure, an asset, a liability, a profit, gain as per the accounting principles is called an account.

Question 3.

State the meaning of the Single Entry System.

Answer:

A book-keeping system in which only one aspect of every business transaction is considered and systematically recorded in the books of accounts and other aspects are completely ignored is called Single Entry System.

![]()

Question 4.

What is Personal Account?

Answer:

Account of person or account relating to a person with whom a business keeps dealings is called Personal Account.

e.g. Kishor’s A/c, Bank of India’s A/c.

Question 5.

State the rules of Nominal Account.

Answer:

The rules of Nominal Account state that Debit all expenses or loses and Credit all incomes and gains.

Question 6.

Give two examples of intangible assets.

Answer:

Goodwill and Patents or Trademark are two examples of intangible assets.

Question 7.

State the meaning of Real Account.

Answer:

Account of tangible as well as intangible property or anything owned and possessed by the business is called real account, e.g. Cash A/c.

Question 8.

Give two examples of income and gains.

Answer:

Interest received, Discount earned, sales, etc. are examples of income and gains.

![]()

Question 9.

State the rule for Personal Account.

Answer:

The rule of personal account states that Debit the receiver and Credit the giver.

Question 10.

How many methods of recording accounting information are there?

Answer:

The methods of recording accounting information are broadly classified as (i) Indian System and (ii) English System. It is sub-classified as (a) a Single Entry System and (b) a Double Entry System.

2. Write one word/term or phrase which can substitute each of the following statements.

Question 1.

Method of Accounting which records both aspects of the transaction.

Answer:

Double Entry System

Question 2.

The right-hand side of an account.

Answer:

Credit side

Question 3.

Name of the account which is debited when proprietor uses business money for personal use.

Answer:

Drawings A/c

Question 4.

Accounts of Assets and Properties.

Answer:

Real A/c

![]()

Question 5.

Accounts of Expenses and Losses and Incomes and Gains.

Answer:

Nominal A/c

Question 6.

The left-hand side of an account.

Answer:

Debit side

Question 7.

The Assets which cannot be seen, touched or felt.

Answer:

Intangible Asset

Question 8.

A person who invented the Double Entry System.

Answer:

Luca D. Bargo Pacioli

Question 9.

Incomplete system of recording business transactions.

Answer:

Single Entry System

Question 10.

A scientific system of recording business transactions.

Answer:

Double Entry system

3. Select the most appropriate alternatives from those given below and rewrite the statements.

Question 1.

International Accounting day is observed on _______________

(a) 10th November

(b) 12th November

(c) 10th December

(d) 15th December

Answer:

(a) 10th November

![]()

Question 2.

Conventional system of accounting is _______________

(a) English entry system

(b) Double entry system

(c) Indian System

(d) None of these

Answer:

(c) Indian System

Question 3.

Every debit has corresponding _______________

(a) Debit

(b) Credit

(c) Right hand side

(d) None of these

Answer:

(b) Credit

Question 4.

Radha’s Account is a type of _______________ account.

(a) Nominal

(b) Personal

(c) Real

(d) Expenses

Answer:

(b) Personal

Question 5.

Machinery Account is _______________ account.

(a) Nominal

(b) Income

(c) Personal

(d) Real

Answer:

(d) Real

![]()

Question 6.

Goodwill is _______________ asset.

(a) Tangible

(b) Current

(c) an intangible

(d) None of these

Answer:

(c) an intangible

Question 7.

Prepaid expenses is _______________ account.

(a) Real

(b) Personal

(c) Nominal

(d) Income

Answer:

(b) Personal

Question 8.

Debit the receiver, Credit the _______________

(a) Goes out

(b) Giver

(c) Income and gains

(d) Comes in

Answer:

(b) Giver

Question 9.

Debit what comes in, Credit what _______________

(a) Giver

(b) Expenses and losses

(c) Goes out

(d) Income and gains

Answer:

(c) Goes out

![]()

Question 10.

Debit all _______________ and Credit all income and gains.

(a) Giver

(b) Expenses and losses

(c) Goes out

(d) None of these

Answer:

(b) Expenses and Losses

4. State whether the following statements are True or False with reasons.

Question 1.

Outstanding expense is a nominal account.

Answer:

This statement is False.

Outstanding expenses are personal accounts. It is a representative personal account. Expenses are payable to some person.

Question 2.

A capital account is a real account.

Answer:

This statement is False.

Capital is a personal account. Amount invested in the business by the proprietor is capital. A proprietor is a natural person.

Question 3.

Every debit has equal and corresponding credit.

Answer:

This statement is True.

Under the Double Entry System, the two-fold effects of each transaction are recorded. Under this system one account is to be debited and another is to be credited with an equal amount.

![]()

Question 4.

The discount received is a nominal account.

Answer:

This statement is True.

Discount received in an income for the business. All expenses and income come under the Nominal account.

Question 5.

The drawings account is a nominal account.

Answer:

This statement is False.

The drawing is a Personal account. Drawing means cash on goods withdrawn by the proprietor for personal use. As the proprietor is a Personal account his drawings are also a Personal account.

Question 6.

Outstanding salary is a nominal account.

Answer:

This statement is False.

Outstanding salary is Personal account. Salary is the amount payable to staff. As he is a person, the amount payable to him is a personal account. It is a Representative Personal account.

Question 7.

A loan account is a personal account.

Answer:

This statement is True.

The loan is taken from a person or bank and they are persons either natural or person or artificial persons.

Question 8.

A goodwill account is a real account.

Answer:

This statement is True.

All properties/assets come under real accounts. Goodwill is an intangible asset so goodwill is a Real account.

Question 9.

A discount account is a nominal account.

Answer:

This statement is False.

Trade discount is a noncash transaction it is not recorded in the books of account so it doesn’t fall under any account.

![]()

Question 10.

Personal transactions of proprietors are recorded in the books of account of business.

Answer:

This statement is False.

Personal transactions of proprietors are not recorded in the books of account of business. Only business transactions are recorded in the books of account of business as businesses have a separate entity.

Question 11.

A motor car account is a Real Account.

Answer:

This statement is True.

All properties and assets fall under real accounts. Motor car is property so it is a real account.

Question 12.

The rule of a Nominal Account is to Debit the receiver and Credit the giver.

Answer:

This statement is False.

The rule of the Nominal account is to debit all expenses and losses Credit all incomes and gains.

Question 13.

A bank loan account is a Nominal account.

Answer:

This statement is False.

The bank account is a Personal account. It is a representative person.

Question 14.

Assets = Capital + Liabilities

Answer:

This statement is True.

Total assets are always equal to total liabilities. Total liabilities include capital also.

So Assets = Capital + Liabilities.

![]()

Question 15.

A Trademark account is a personal account.

Answer:

This statement is False.

Trademark is a real account. All tangible and intangible assets are properties and they fall under real account.

5. Fill in the blanks.

Question 1.

Increase in asset is debited and decrease in asset is _______________

Answer:

Credited

Question 2.

Assets = Liabilities + _______________

Answer:

Capital

Question 3.

Increase in capital is credited and decrease in capital is _______________

Answer:

Debited

Question 4.

Scientific and complete system of recording is known as _______________

Answer:

Double Entry System

Question 5.

Debit all expenses and losses, Credit all _______________

Answer:

Income and Gains

![]()

Question 6.

Land and Building account is _______________ account.

Answer:

Real

Question 7.

Cash Book and Personal Accounts are only maintained under _______________ system.

Answer:

Single Entry

Question 8.

Debit what comes in and credit what goes out is the rule of _______________ account.

Answer:

Real

Question 9.

Travelling expenses account is _______________ type of Account.

Answer:

Nominal

Question 10.

Every transaction has _______________ effect.

Answer:

Two Fold

Question 11.

_______________ accounts are accounts of properties and assets.

Answer:

Real

![]()

Question 12.

Laptop account is a _______________ account.

Answer:

Real

6. Classify the following accounts under the types of Personal, Real, and Nominal accounts.

Question 1.

Mr. Rohit’s capital A/c

Answer:

Personal Account

Question 2.

Loose Tools A/c

Answer:

Real Account

Question 3.

Drawing A/c

Answer:

Personal Account

Question 4.

Cartage A/c

Answer:

Nominal Account

Question 5.

Prepaid Rent A/c

Answer:

Personal Account

![]()

Question 6.

Copyright A/c

Answer:

Real Account

Question 7.

Patent A/c

Answer:

Real Account

Question 8.

Outstanding Income A/c

Answer:

Personal Account

Question 9.

Prepaid Expenses A/c

Answer:

Personal Account

Question 10.

Commission Received A/c

Answer:

Nominal Account

Question 11.

Freight A/c

Answer:

Nominal Account

![]()

Question 12.

Plant and Machinery A/c

Answer:

Real Account

Question 13.

Sundry Income A/c

Answer:

Nominal Account

Question 14.

Live Stock A/c

Answer:

Real Account

Question 15.

Goods distributed as free sample A/c

Answer:

Nominal Account

Question 16.

Radhika’s A/c

Answer:

Personal Account

![]()

Question 17.

Outstanding Wages A/c

Answer:

Personal Account

Question 18.

Loss on Sale of Furniture A/c

Answer:

Nominal Account

Question 19.

Bank of Maharashtra A/c

Answer:

Personal Account

Question 20.

Loan A/c

Answer:

Personal Account

Question 21.

Computer A/c

Answer:

Real Account

Question 22.

Legal Expenses A/c

Answer:

Nominal Account

![]()

Question 23.

Fixed Deposit A/c

Answer:

Real Account

Question 24.

Income Receivable A/c

Answer:

Personal Account

Question 25.

Audit Fees A/c

Answer:

Nominal Account

Question 26.

Trademark A/c

Answer:

Real Account

Question 27.

Loss by fire A/c

Answer:

Nominal Account

Question 28.

Motor Car A/c

Answer:

Real Account

![]()

Question 29.

Income tax A/c

Answer:

Personal Account

Question 30.

GST A/c (Goods and Service Tax)

Answer:

Nominal Account

Question 31.

Siddhivinayak Trust A/c

Answer:

Personal Account

Question 32.

Office Equipment A/c

Answer:

Real Account

Question 33.

The stock of Stationery A/c

Answer:

Real Account

Question 34.

Indian Railways A/c

Answer:

Personal Account

![]()

Question 35.

Income Received in Advance A/c

Answer:

Personal Account

Question 36.

Dividend on Investment Advance A/c

Answer:

Nominal Account

Question 37.

Discount A/c

Answer:

Nominal Account

Question 38.

Raj & company A/c

Answer:

Personal Account

![]()

Question 39.

Repairs A/c

Answer:

Nominal Account

Question 40.

Royalty A/c

Answer:

Nominal Account

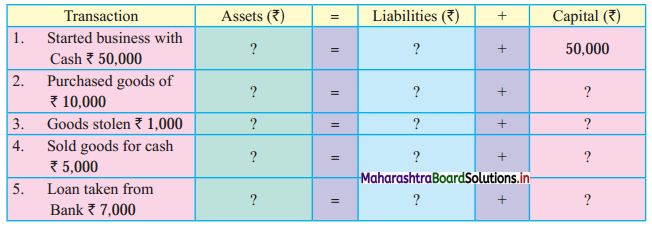

7. Complete the following Accounting equation table.

Question 1.

Answer:

| Transactions | Assets (₹) | = | Liabilities (₹) | + | Capital (₹) |

| 1. Started business with Cash ₹ 50,000 | 50,000 | = | 00 | + | 50,000 |

| 2. Purchased goods of ₹ 10,000 | 50,000 (+) 10,000 (-) 10,000 |

= | 00 | + | 50,000 |

| 3. Goods stolen ₹ 1,000 | 50,000 (-) 1,000 |

= | 00 | + | 50,000 (-) 1,000 |

| 4. Sold goods for Cash ₹ 5,000 | 49,000 (+) 5,000 (-) 5,000 |

= | 00 | + | 49,000 |

| 5. Loan taken from Bank ₹ 7,000 | 49,000 (+) 7,000 |

= | 00 7,000 |

+ | 49,000 |

| Total | 56,000 | = | 7,000 | + | 49,000 |

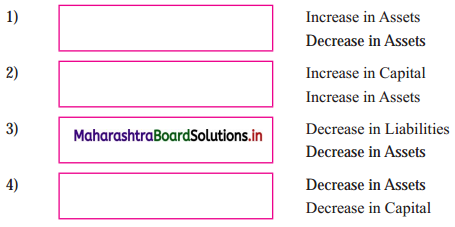

8. Give necessary transactions for the following effect of increase and decrease in Assets, Capital, and Liabilities.

Question 1.

Answer:

| 1. | Sold goods for Cash ₹ 10,000 | Increase in Assets Decrease in Assets |

| 2. | Goods costing ₹ 12,000 Sold for ₹ 15,000 | Increase in Capital Decrease in Assets |

| 3. | Paid cash ₹ 8,500 to our creditor Mr. Kishor | Decrease in Liabilities Decrease in Assets |

| 4. | Goods worth ₹ 7,000 stolen from Godown | Decrease in Assets Decrease in Capital |

Practical Problems

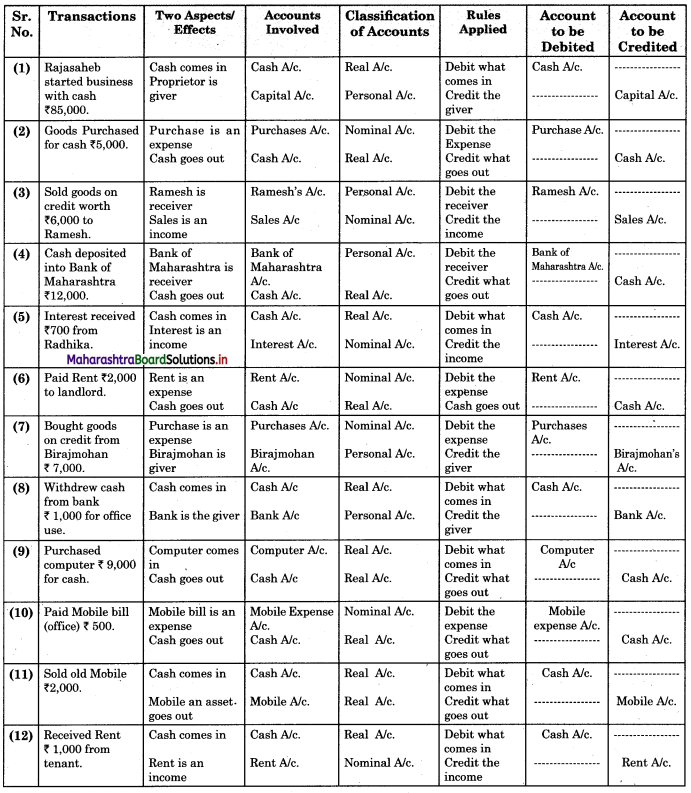

Question 1.

Prepare a chart showing Analysis of the following transactions in a Tabular form according to the Traditional Approach:

1. Rajasaheb started the business with cash of ₹ 85,000.

2. Goods Purchased for cash ₹ 5,000.

3. Sold goods on credit worth ₹ 6,000 to Ramesh.

4. Cash deposited into Bank of Maharashtra ₹ 12,000.

5. Interest received ₹ 700 from Radhika.

6. Paid Rent ₹ 2,000 to the landlord.

7. Bought goods on credit from Birajmohan ₹ 7,000.

8. Withdrew cash from bank ₹ 1,000 for office use.

9. Purchased computer ₹ 9,000 for cash.

10. Paid Mobile bill (office) ₹ 500.

11. Sold old Mobile ₹ 2,000.

12. Received Rent ₹ 1,000 from the tenant.

Solution:

Table showing analysis of the transactions is given below (Traditional Approach)

![]()

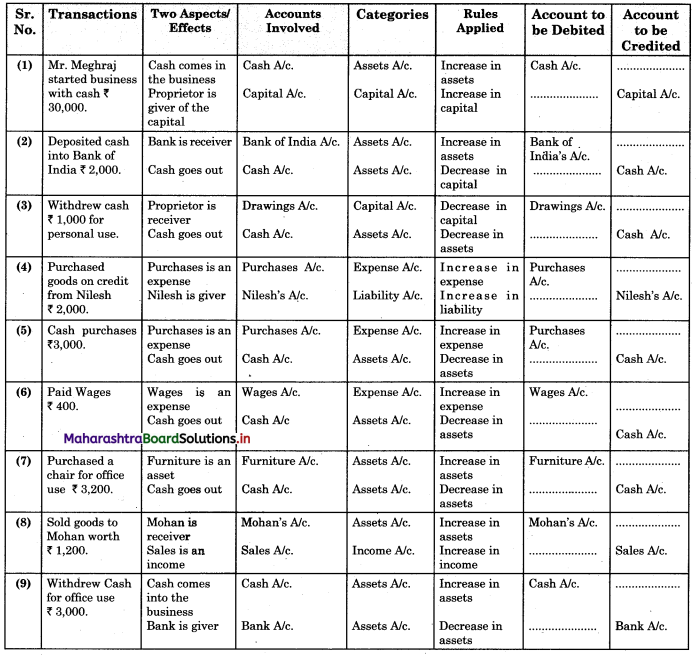

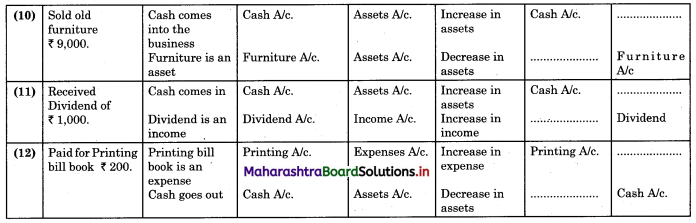

Question 2.

Prepare Chart showing Analysis of the following transaction in a Tabular form according to Modern Approach.

1. Mr. Meghraj started the business with cash of ₹ 30,000.

2. Deposited cash into Bank of India ₹ 2,000.

3. Withdrew cash ₹ 1,000 for personal use.

4. Purchased goods on credit from Nilesh ₹ 2,000.

5. Cash purchases ₹ 3,000.

6. Paid Wages ₹ 400.

7. Purchased a chair for office use ₹ 3,200.

8. Sold goods to Mohan worth ₹ 1,200.

9. Withdrew Cash for Office use ₹ 3,000.

10. Sold old furniture ₹ 9,000.

11. Received Dividend of ₹ 1,000.

12. Paid for Printing bill book ₹ 200.

Solution:

Analysis of transactions by applying rules of Debit and Credit (Modern Approach)

Question 3.

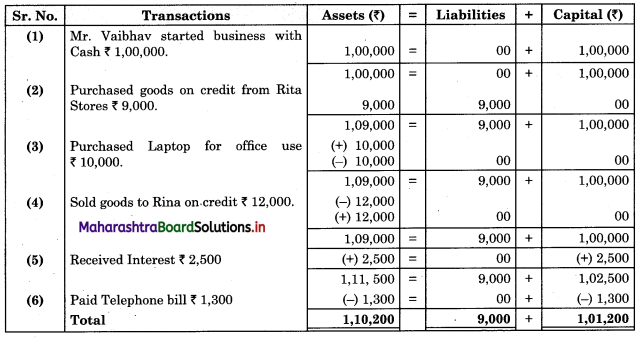

Give the accounting equation for the following transactions:

1. Mr. Vaibhav started the business with Cash of ₹ 1,00,000.

2. Purchased goods on credit from Rita Stores ₹ 9,000.

3. Purchased Laptop for office use ₹ 10,000.

4. Sold goods to Rina on credit ₹ 12,000.

5. Received Interest ₹ 2,500.

6. Paid Telephone bill ₹ 1,300.

Solution:

Table showing Accounting equations for the transactions.

![]()

Question 4.

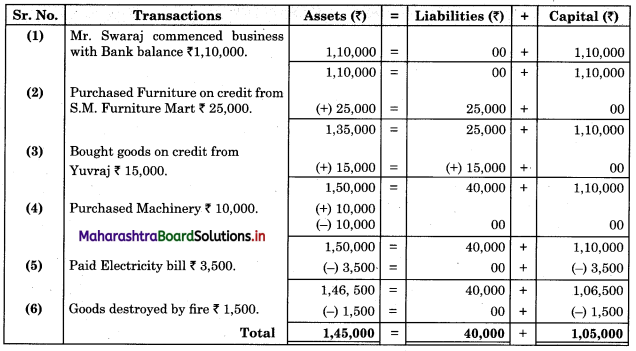

Give the accounting equation for the following transactions.

1. Mr. Swaraj commenced business with a Bank balance of ₹ 1,10,000.

2. Purchased Furniture on credit from S.M Furniture Mart ₹ 25,000.

3. Bought goods on credit from Yuvraj ₹ 15,000.

4. Purchased Machinery ₹ 10,000.

5. Paid Electricity bill ₹ 3,500.

6. Goods destroyed by fire ₹ 1,500.

Solution:

Table showing equation for the transactions.

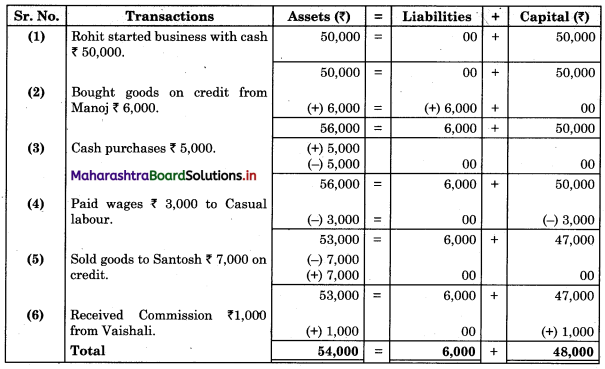

Question 5.

Show accounting equation for the following transactions:

1. Rohit started the business with cash of ₹ 50,000.

2. Bought goods on credit from Manoj ₹ 6,000.

3. Cash purchases ₹ 5,000.

4. Paid wages ₹ 3,000 to Casual labour.

5. Sold goods to Santosh ₹ 7,000 on credit.

6. Received Commission ₹ 1,000 from Vaishali.

Solution:

Class 11 Commerce BK Textbook Solutions Digest

- 11th Bk Chapter 1 Practical Problems

- 11th Bk Chapter 2 Practical Problems

- 11th Bk Chapter 3 Practical Problems

- 11th Bk Chapter 4 Practical Problems

- 11th Bk Chapter 5 Practical Problems

- 11th Bk Chapter 6 Practical Problems

- 11th Bk Chapter 7 Practical Problems

- 11th Bk Chapter 8 Practical Problems

- 11th Bk Chapter 9 Practical Problems

- 11th Bk Chapter 10 Practical Problems